The 8615 instructions can be subdivided into different sections as well. For example, many companies want to know and evaluate the amount of cash they collected from sales, credit customers, and other sources. A single disadvantage of the cash receipts journal is that it only considers the cash basis of accounting. It doesn’t consider the accrual basis of accounting which is the principal basis of doing double-entry bookkeeping and prudent accounting. The cash receipts journal manages all cash inflows of a business organization.

Cash sale

Just like everything else in accounting, there’s a particular way to make an accounting journal entry when recording debits and credits. Double entry system of bookkeeping says that every transaction affects two accounts. There is a proper procedure for recording each financial transaction in this system, called as accounting process.The process starts from journal followed by ledger, trial balance, and final accounts.

AccountingTools

Again, you must record a debit in your cash receipts journal and a credit in your sales journal. All cash transactions made during an accounting period are documented in a cash receipts journal, which is set up as a subsidiary of the general ledger. Chronological entries are made in the cash receipts journal and the balance is continuously updated and confirmed.

Single Column Cash Book

Similarly, it also provides an easy way to keep track of all the unpaid supplier and vendor payments by allowing the business to quickly see what cash was received and paid out during a said period. The Supreme Court has authority to appoint a successor signatory for the attorney trust account. Thelawyer must safeguard and segregate those assets from the lawyer's personal,business or other assets. The three column cashbook is sometimes referred to as the triple cashbook, treble cashbook or the 3 column cashbook.

Record Retention for Businesses

Credit sales are handled using the accrual basis of accounting, while cash transactions are handled using the cash basis. Another Loan taken by an individual from any bank or financial institution is also recorded in the cash receipts journal. Both cash and credit sales of non-inventory or merchandise are recorded in the general journal.

You may choose any recordkeeping system suited to your business that clearly shows your income and expenses. The business you are in affects the type of records you need to keep for federal tax purposes. Your recordkeeping system should also include a summary of your business transactions.

As with other journals, the cash receipts journal is posted in two stages. Any entries in the accounts receivable column should be posted to the subsidiary accounts receivable ledger on a daily basis. The credit columns in a cash receipts journal will most often include both accounts receivable and sales. Again, other columns can be used depending on the type of routine transactions that the firm engages in. Because you have already received the cash at the point of sale, you can record it in your books.

Double Entry Bookkeeping is here to provide you with free online information to help you learn and understand bookkeeping and introductory accounting. Depending on how frequently you get cash from customers, there can be a lot of entries in this journal. My Accounting Course is a world-class educational resource developed by experts to simplify accounting, finance, & investment analysis topics, so students and professionals can learn and propel their careers. We follow strict ethical journalism practices, which includes presenting unbiased information and citing reliable, attributed resources. A check is placed under the total of this column as this total is net posted.

As an accounting entry that records the receipt of money from a customer, a cash sales receipt is a debit. The cash disbursement diary and the cash receipts journal are typically divided. In contrast to a cash account, which is an account within a general ledger, a cash receipts journal is a separate ledger. And that is that it only takes into consideration the cash basis of accounting.

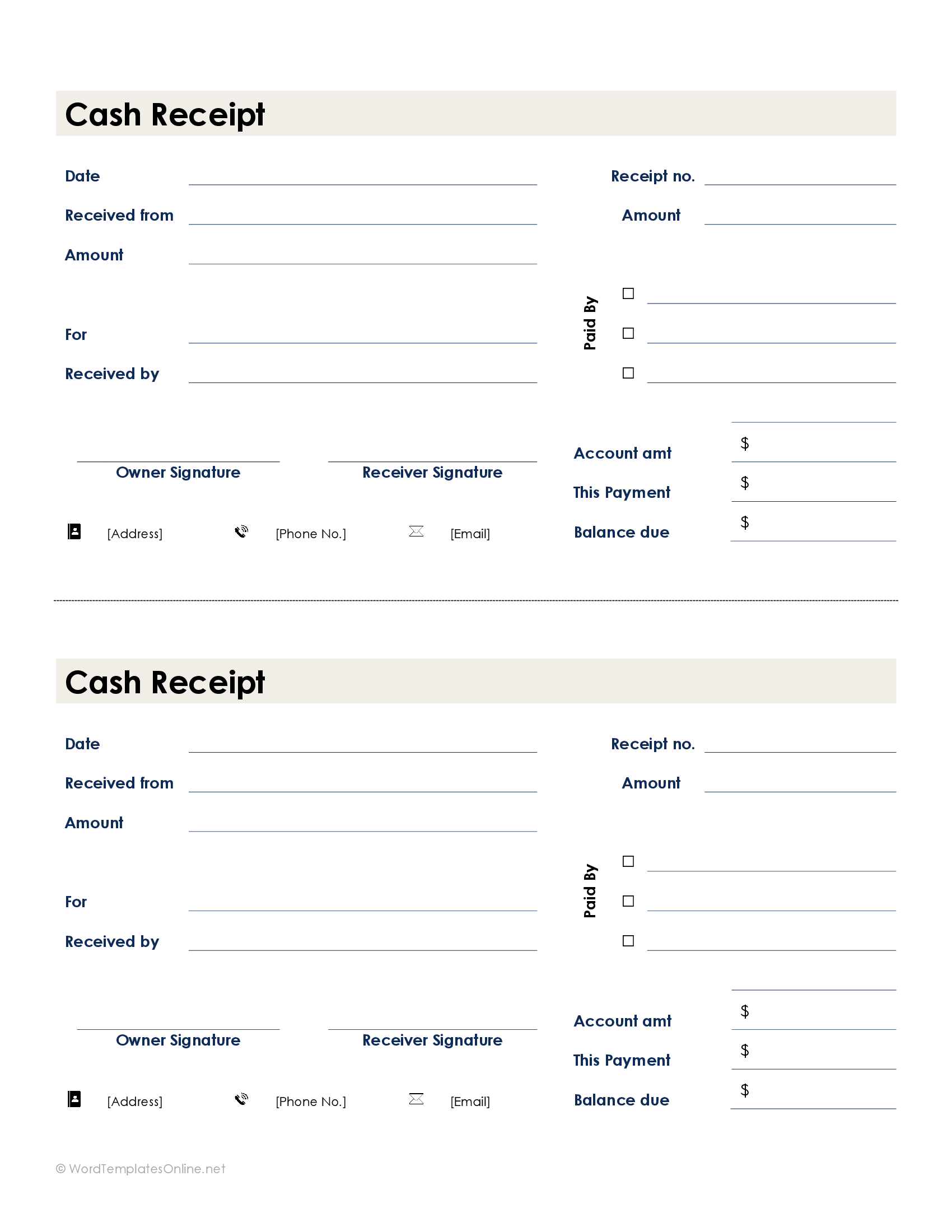

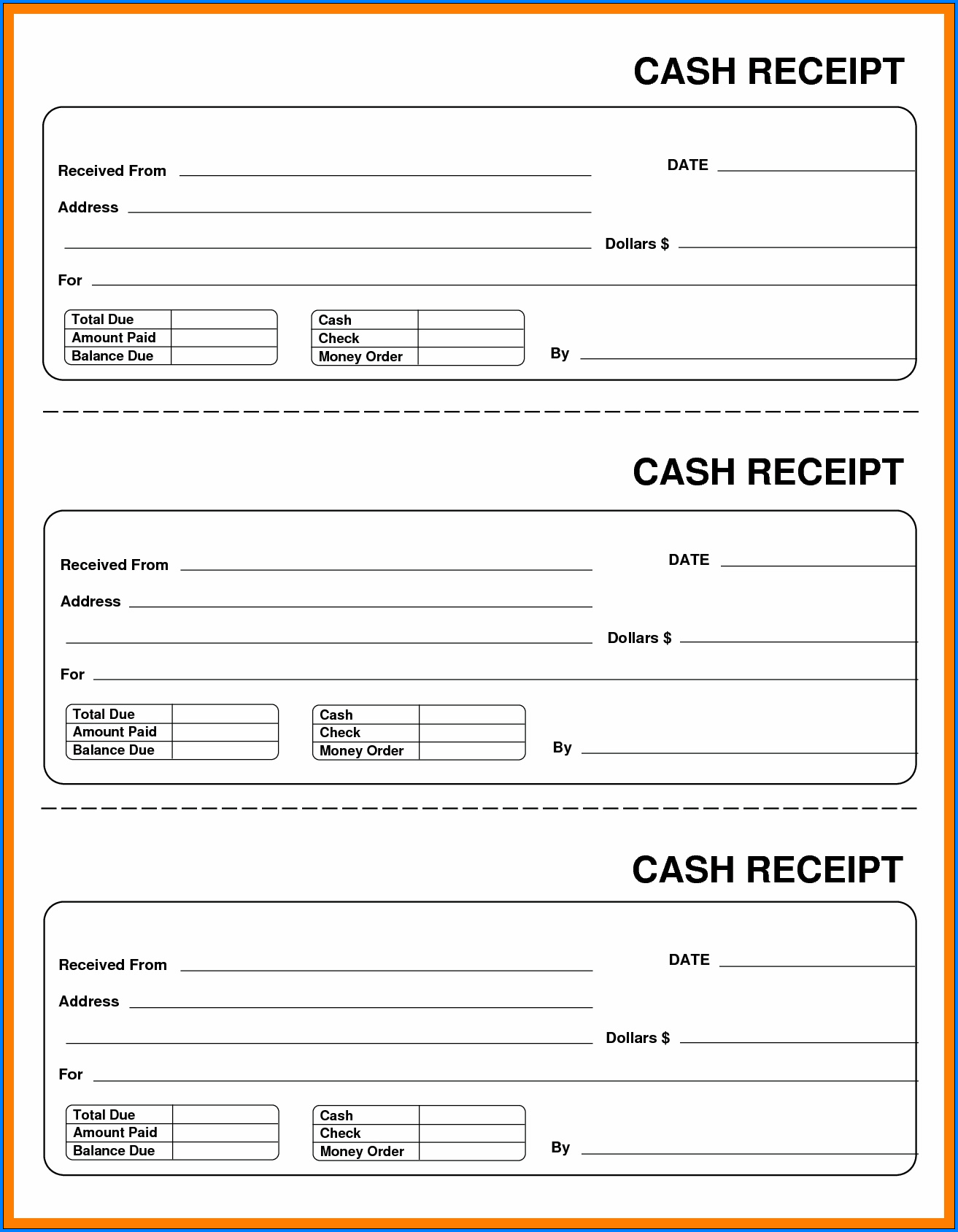

- A cash receipts journal is a subsidiary ledger in which cash sales are recorded.

- There is a proper procedure for recording each financial transaction in this system, called as accounting process.The process starts from journal followed by ledger, trial balance, and final accounts.

- Notice that only credit sales of inventory and merchandise items are recorded in the sales journal.

- Each transaction is documented with its date, description, invoice number (if applicable), and the amount received in the cash account column.

Special journals (in the field of accounting) are specialized lists of financial transaction records which accountants call journal entries. In contrast to a general journal, each special journal records transactions of a specific type, such as sales or purchases. Cost of sales is also known as the cost of goods sold, and the two terms are used interchangeably. Generally in the cash receipts journal to debit columns for cash receipts and cash discount and three credit columns for accounts receivable, sales and other accounts are there. Cash received from various sources other than cash sales and account receivables are recorded in other accounts column.