As a company grows, it may have learned ways to produce more without a need to increase its expenses, resulting in a higher revenue stream. However, a favorable variance may indicate that production expectations tax definition were not realistic in the first place, which is more likely if the company is new. Note 10.26 "Business in Action 10.2" illustrates just howimportant it is to track direct materials variances accurately.

6 Direct Materials Variances

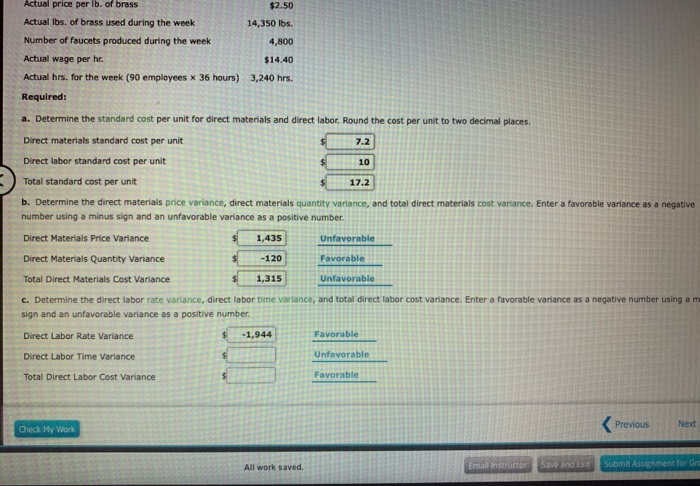

The direct materials used in production cost more than was anticipated, which is an unfavorable outcome. In other words, when actual quantity of materials used deviates from the standard quantity of materials allowed to manufacture a certain number of units, materials quantity variance occurs. The direct materials quantity variance of Blue Sky Company, as calculated above, is favorable because the actual quantity of materials used is less than the standard quantity allowed. In a manufacturing company, the purchasing and accounting departments usually set a standard price for materials meeting certain engineering specifications. When setting a standard price, they consider factors such as market conditions, vendors’ quoted prices, and the optimum size of a purchase order. A direct materials cost variance (sometimes called a materials price variance or MPV) occurs when a company pays a higher or lower price than the standard price set for materials.

Direct Materials Price Variance

By delving into the specifics of variances, companies can uncover inefficiencies and make informed decisions to optimize their operations. The first step in this analysis is to regularly review variance reports, which provide a snapshot of how actual costs compare to standard costs. These reports should be detailed and timely, allowing managers to quickly identify and address any discrepancies. Reliable suppliers who consistently deliver quality materials at agreed-upon prices help maintain stable production costs.

- The business has only been running for about six months but has proven popular internationally because of the customization process and the good quality fabric you use.

- The materials quantity variancefocuses on the quantity of materials used in production.

- You buy in bulk but after three months, the price dramatically increases, something you had not counted on.

Great! The Financial Professional Will Get Back To You Soon.

Direct material price variance is the difference between what was actually spent on the raw materials purchased during a period and the standard cost that would apply if the materials were bought at the standard rate. To calculate the variance, we multiply the actual purchase volume by the standard and actual price difference. Analyzing direct material variance is a powerful tool for businesses aiming to maintain cost control and enhance profitability.

If a company's actual quantity used exceeds the standard allowed, what would the variance be?

As a result of this unfavorable outcome information, the company may consider using cheaper materials, changing suppliers, or increasing prices to cover costs. As you calculate variances, youshould think through the variance to confirm whether it isfavorable or unfavorable. Direct materials quantity variance is a part of the overall materials cost variance that occurs due to the difference between the actual quantity of direct materials used and the standard quantity allowed for the output. The difference column shows that 200 fewer pounds were used than expected (favorable). It also shows that the actual price per pound was $0.30 higher than standard cost (unfavorable).

If more than 600 tablespoons of butter were used, management would investigate to determine why. Let’s say your custom blankets are made of a rich acrylic and polyester blend that keeps the blanket soft for years. You buy in bulk but after three months, the price dramatically increases, something you had not counted on. As a result you are spending more than expected on materials, and this price variance is costing you. Now when you look at your financial statements you see an unfavorable variance.

Specifically, knowing the amount and direction of the difference for each can help them take targeted measures forimprovement. In the first six months of 2004, steelprices increased 76 percent, from $350 a ton to $617 a ton. Forauto suppliers that use hundreds of tons of steel each year, thishad the unexpected effect of increasing expenses and reducingprofits. For example, a major producer of automotive wheels had toreduce its annual earnings forecast by $10,000,000 to $15,000,000as a result of the increase in steel prices.

Technological advancements and automation also influence direct material variance. The integration of advanced technologies, such as IoT and AI, into the production process can provide real-time data on material usage and identify inefficiencies. For example, IoT sensors can monitor the exact amount of material used in each production cycle, allowing for precise adjustments and reducing waste. AI algorithms can analyze historical data to predict future material needs more accurately, helping businesses plan better and avoid unexpected variances. Note that both approaches—the direct materials quantity variancecalculation and the alternative calculation—yield the sameresult. The standard quantity of 420,000 pounds is the quantity ofmaterials allowed given actual production.

These thin margins are the reason autosuppliers examine direct materials variances so carefully. Anyunexpected increase in steel prices will likely cause significantunfavorable materials price variances, which will lead to lowerprofits. Auto part suppliers that rely on steel will continue toscrutinize materials price variances and materials quantityvariances to control costs, particularly in a period of risingsteel prices. Recall from Figure 10.1 that the direct materials standard pricefor Jerry’s is $1 per pound, and the standard quantity of directmaterials is 2 pounds per unit. Figure 10.4 shows how to calculatethe materials price and quantity variances given the actual resultsand standards information.

The difference between this actual expenditure and the actual expenditure on direct material is the direct materials price variance. The standard price of materials purchased by Angro is $2.00 per kg and standard quantity of materials allowed to produce a unit of product is 1.5kg. During December 2020, 5,000 units were produced using 8,000kgs of direct materials. Calculate direct materials quantity variance and also indicate whether it is favorable or unfavorable.

The total direct materials cost variance is also found by combining the direct materials price variance and the direct materials quantity variance. By showing the total materials variance as the sum of the two components, management can better analyze the two variances and enhance decision-making. In this case, the actual quantity of materials used is 0.50 pounds, the standard price per unit of materials is $7.00, and the standard quantity used is 0.25 pounds. This is an unfavorable outcome because the actual quantity of materials used was more than the standard quantity expected at the actual production output level. As a result of this unfavorable outcome information, the company may consider retraining workers to reduce waste or change their production process to decrease materials needs per box.